Synergistic Impacts of China’s Subsidy Policy and New Energy Vehicle Credit Regulation on the Technological Development of Battery Electric Vehicles

Abstract

:1. Introduction

2. Materials and Methods

2.1. Materials

2.1.1. The Rationale of China’s Subsidy Schemes

2.1.2. The Rationale of China’s NEV Credit Regulation

2.1.3. Theoretical Analysis of the Chinese BEV Market

2.2. Methods

2.2.1. Average Electricity Consumption Rate

2.2.2. Vehicle Cost Model

2.2.3. Contribution Rate of Subsidy

2.2.4. Credit Cost-Effectiveness

3. Results

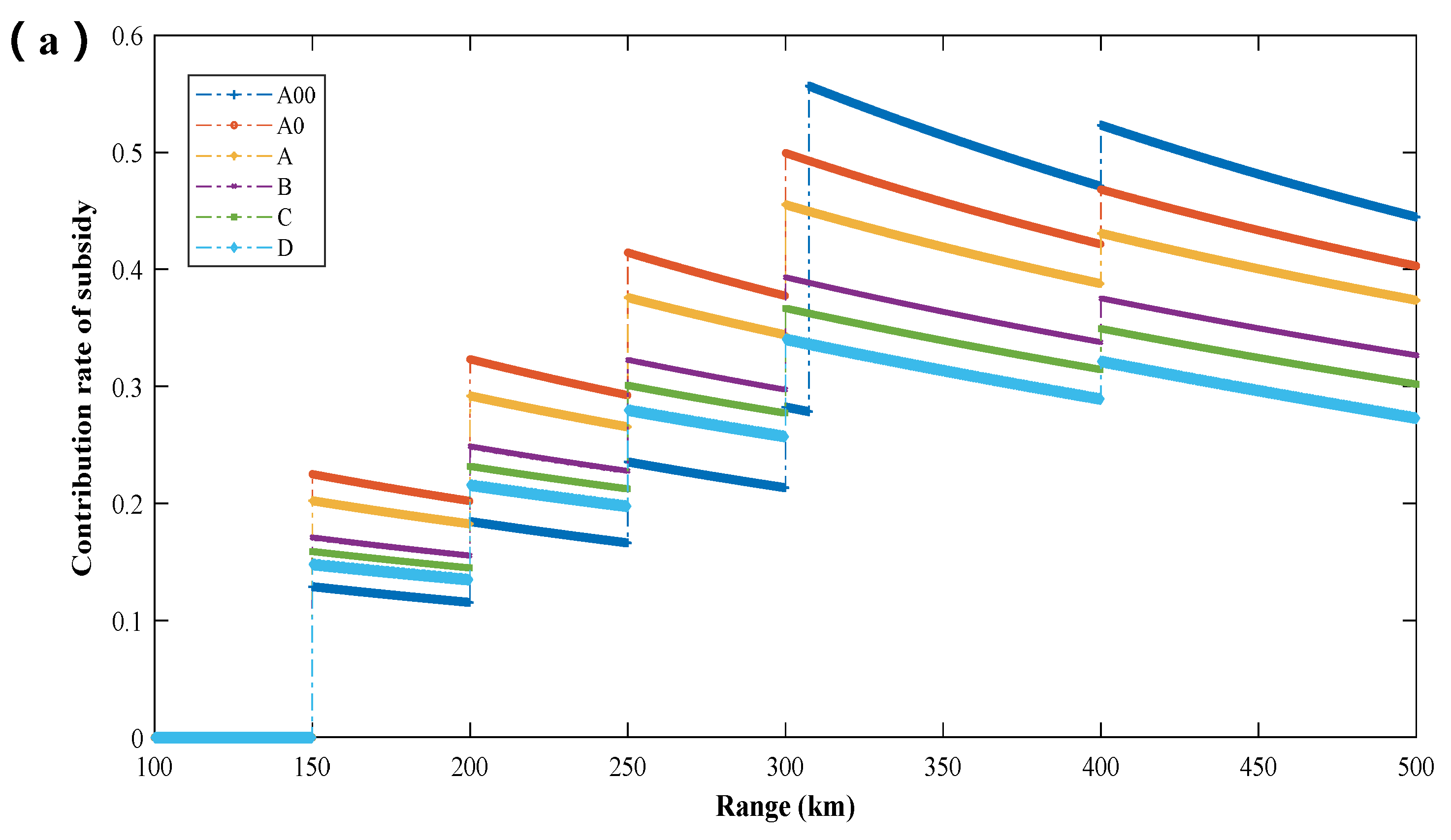

3.1. Contribution Rate of Subsidy

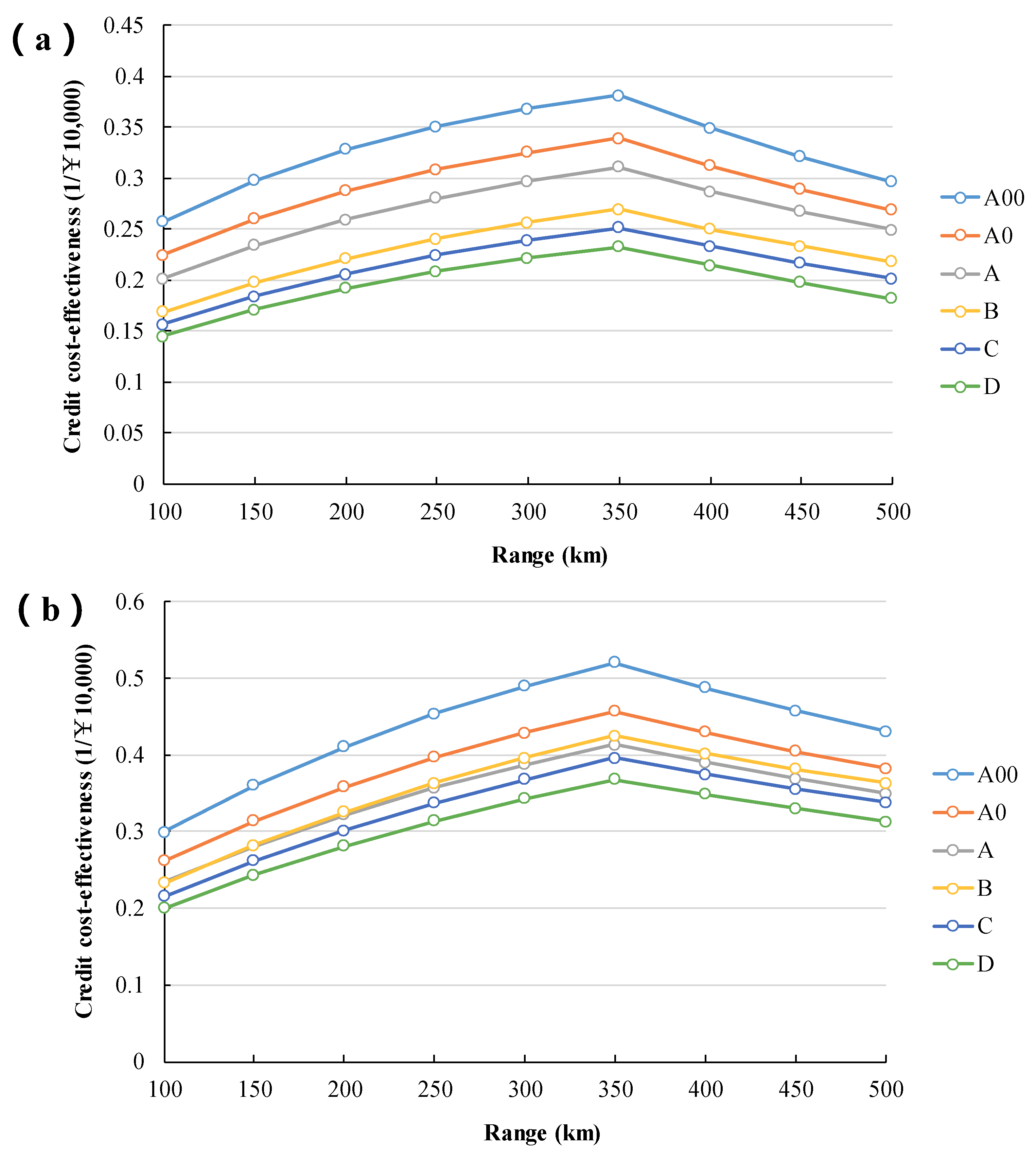

3.2. Credit Cost-Effectiveness under the NEV Credit Regulation

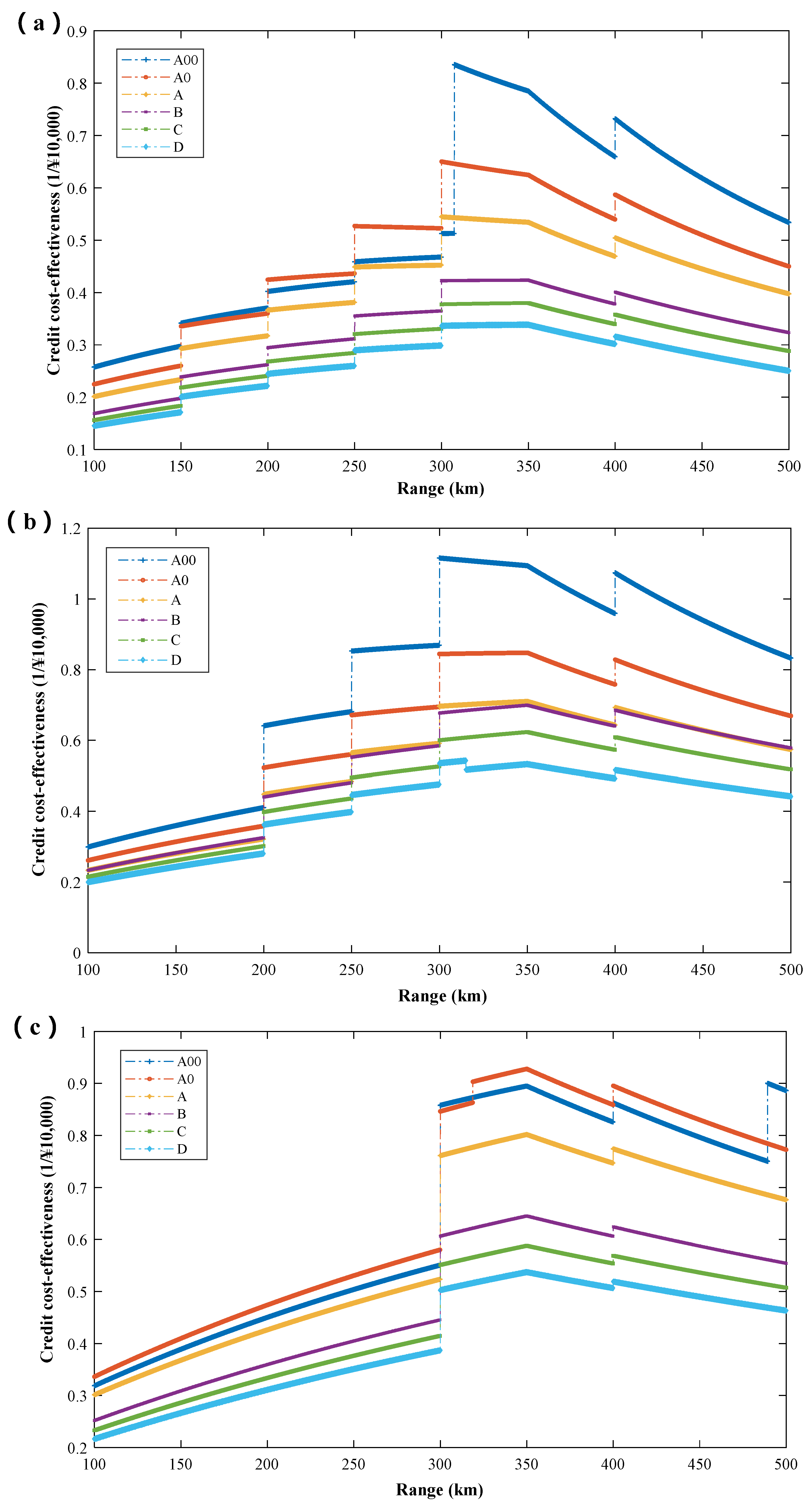

3.3. Credit Cost-Effectiveness under the Subsidy Scheme and NEV Credit Regulation

4. Discussion and Policy Implications

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Abbreviations

| AER | All-Electric Range |

| BEV | Battery Electric Vehicle |

| CAFC | Corporate Average Fuel Consumption |

| CAFE | Corporate Average Fuel Economy |

| CATC | China Automotive Test Cycle |

| EPA | Environmental Protection Agency |

| EV | Electric Vehicle |

| FCV | Fuel Cell Vehicle |

| ICE | Internal Combustion Engine |

| MIIT | Ministry of Industry and Information Technology |

| MSRP | Manufacturer’s Suggested Retail Price |

| NEDC | New European Driving Cycle |

| NEV | New Energy Vehicle |

| NHTSA | National Highway Traffic Safety Administration |

| OEM | Original Equipment Manufacturer |

| PC | Passenger Car |

| PEV | Plug-in Electric Vehicle |

| PHEV | Plug-in Hybrid Electric Vehicle |

| PM | Particulate Matter |

| ZEV | Zero Emission Vehicle |

References

- CAAM; CATARC; Toyota. Annual Report on Automotive Industry in China (2018); Social Sciences Academic Press: Beijing, China, 2018. [Google Scholar]

- Hao, H.; Geng, Y.; Wang, H.; Ouyang, M. Regional disparity of urban passenger transport associated GHG (greenhouse gas) emissions in China: A review. Energy 2014, 68, 783–793. [Google Scholar] [CrossRef]

- Wang, H.; Zhang, X.; Ouyang, M. Energy consumption of electric vehicles based on real-world driving patterns: A case study of Beijing. Appl. Energy 2015, 157, 710–719. [Google Scholar] [CrossRef]

- ETRI. Oil and Gas Industry Development Report at Home and Abroad in 2017; Petroleum Industry Press: Beijing, China, 2018. [Google Scholar]

- IEA. World Energy Outlook Special Report 2015: Energy and Climate Change. 2015. Available online: https://www.iea.org/publications/freepublications/publication/WEO2015SpecialReportonEnergyandClimateChange.pdf (accessed on 18 September 2018).

- Zhao, F.; Hao, H.; Liu, Z. Technology strategy to meet China’s 5 L/100 km fuel consumption target for passenger vehicles in 2020. Clean Technol. Environ. Policy 2016, 18, 7–15. [Google Scholar] [CrossRef]

- Chen, L.; Zhang, H.; Guo, Y. Estimating the economic cost of emission reduction in Chinese vehicle industry based on multi-objective programing. Clean Technol. Environ. Policy 2013, 15, 727–734. [Google Scholar] [CrossRef]

- De Schepper, E.; Van Passel, S.; Lizin, S.; Achten, W.M.; Van Acker, K. Cost-efficient emission abatement of energy and transportation technologies: Mitigation costs and policy impacts for Belgium. Clean Technol. Environ. Policy 2014, 16, 1107–1118. [Google Scholar] [CrossRef]

- CAAM. Press Conference. 2018. Available online: http://nev.ofweek.com/2018-01/ART-71008-12008-30188460.html (accessed on 15 February 2018).

- State Council. Industry Development Plan of Energy Saving and New Energy Vehicles 2012–2020. 2012. Available online: http://www.gov.cn/zhengce/content/2012-07/09/content_3635.htm (accessed on 15 February 2018).

- MIIT. Technology Roadmap for Energy Saving and New Energy Vehicles; China Machine Press: Beijing, China, 2016. [Google Scholar]

- Zhou, Y.; Wang, M.; Hao, H.; Johnson, L.; Wang, H. Plug-in electric vehicle market penetration and incentives: A global review. Mitig. Adapt. Strateg. Glob. Chang. 2015, 20, 777–795. [Google Scholar] [CrossRef]

- Hao, H.; Ou, X.; Du, J.; Wang, H.; Ouyang, M. China’s electric vehicle subsidy scheme: Rationale and impacts. Energy Policy 2014, 73, 722–732. [Google Scholar] [CrossRef]

- MIIT. The Parallel Scheme of Corporate Average Fuel Consumption of the Passenger Car and New Energy Vehicle Credits. 2017. Available online: http://www.miit.gov.cn/n1146290/n4388791/c5826378/content.html (accessed on 15 February 2018).

- Wang, Y.; Zhao, F.; Yuan, Y.; Hao, H.; Liu, Z. Analysis of Typical Automakers’ Strategies for Meeting the Dual-Credit Regulations Regarding CAFC and NEVs. Automot. Innov. 2018, 1, 15–23. [Google Scholar] [CrossRef] [Green Version]

- Internal Revenue Service. Plug-In Electric Drive Vehicle Credit. Available online: http://www.irs.gov/Businesses/Plug-In-Electric-Vehicle-Credit-%28IRC-30-and-IRC-30D%29 (accessed on 18 September 2018).

- ACEA. ACEA Tax Guide; ACEA: Brussels, Belgium, 2015. [Google Scholar]

- JAMA. Fact Sheet—Japanese Government Incentives for the Purchase of Environmentally Friendly Vehicles; Japan Automobile Manufacturers Association: Tokyo, Japan, 2010. [Google Scholar]

- China Automotive Technology & Research Center. Development Report on New Energy Vehicle Industry of China; Social Sciences Academic Press: Beijing, China, 2016. [Google Scholar]

- Hardman, S.; Chandan, A.; Tal, G.; Turrentine, T. The effectiveness of financial purchase incentives for battery electric vehicles–A review of the evidence. Renew. Sustain. Energy Rev. 2017, 80, 1100–1111. [Google Scholar] [CrossRef]

- Hall, D.; Moultak, M.; Lutsey, N. Electric Vehicle Capitals of the World: Demonstrating the Path to Electric Drive; International Council on Clean Transportation: Washington, DC, USA, 2017. [Google Scholar]

- Shafiei, E.; Davidsdottir, B.; Fazeli, R.; Leaver, J.; Stefansson, H.; Asgeirsson, E.I. Macroeconomic effects of fiscal incentives to promote electric vehicles in Iceland: Implications for government and consumer costs. Energy Policy 2018, 114, 431–443. [Google Scholar] [CrossRef]

- Sen, B.; Noori, M.; Tatari, O. Will Corporate Average Fuel Economy (CAFE) Standard help? Modeling CAFE’s impact on market share of electric vehicles. Energy Policy 2017, 109, 279–287. [Google Scholar] [CrossRef]

- Palmer, K.; Tate, J.E.; Wadud, Z.; Nellthorp, J. Total cost of ownership and market share for hybrid and electric vehicles in the UK, US and Japan. Appl. Energy 2018, 209, 108–119. [Google Scholar] [CrossRef]

- Lévay, P.Z.; Drossinos, Y.; Thiel, C. The effect of fiscal incentives on market penetration of electric vehicles: A pairwise comparison of total cost of ownership. Energy Policy 2017, 105, 524–533. [Google Scholar] [CrossRef]

- Harvey, L.D. Cost and energy performance of advanced light duty vehicles: Implications for standards and subsidies. Energy Policy 2018, 114, 1–12. [Google Scholar] [CrossRef]

- California Air Resource Board (CARB). Zero-Emission Vehicle Legal and Regulatory Activities and Background. 2014. Available online: https://www.arb.ca.gov/msprog/zevprog/zevregs/zevregs.htm (accessed on 18 September 2018).

- CARB. Zero Emission Vehicle Credits. 2015. Available online: https://www.arb.ca.gov/msprog/zevprog/zevcredits/2015zevcredits.htm (accessed on 18 September 2018).

- China EV100. Tracking and Evaluation of Major New Energy Vehicle Market Policies in the World; China EV100 Forum: Beijing, China, 2016. [Google Scholar]

- CARB. California exhaust emission standards and test procedures for 2009 through 2017 model zero-emission vehicles and hybrid electric vehicles, in the passenger car, light-duty truck and medium-duty vehicle classes. 2012. Available online: https://www.arb.ca.gov/regact/2012/zev2012/zevpt2.pdf (accessed on 18 September 2018).

- Sierzchula, W.; Nemet, G. Using patents and prototypes for preliminary evaluation of technology-forcing policies: Lessons from California’s Zero Emission Vehicle regulations. Technol. Forecast. Soc. Chang. 2015, 100, 213–224. [Google Scholar] [CrossRef]

- CARB. 2015 Zero Emission Vehicle Credits. 2016. Available online: https://www.arb.ca.gov/msprog/zevprog/zevcredits/2015zevcredits.htm (accessed on 18 September 2018).

- CARB. California Exhaust Emission Standards and Test Procedures for 2018 and Subsequent Model Zero-Emission Vehicles and Hybrid Electric Vehicles, in the Passenger Car, Light-Duty Truck and Medium-Duty Vehicle Classes. 2012. Available online: https://www.arb.ca.gov/msprog/levprog/cleandoc/2018+%20my%20hevtps_clean%20complete_12-12.pdf (accessed on 18 September 2018).

- Greene, D.L.; Park, S.; Liu, C. Public policy and the transition to electric drive vehicles in the US: The role of the zero emission vehicles mandates. Energy Strat. Rev. 2014, 5, 66–77. [Google Scholar] [CrossRef]

- Wesseling, J.H.; Farla, J.C.M.; Hekkert, M.P. Exploring car manufacturers’ responses to technology-forcing regulation: The case of California’s ZEV mandate. Environ. Innov. Soc. Trans. 2015, 16, 87–105. [Google Scholar] [CrossRef]

- Leard, B.; McConnell, V. New Markets for Pollution and Energy Efficiency: Credit Trading under Automobile Greenhouse Gas and Fuel Economy Standards. 2015. Available online: https://ssrn.com/abstract=2622698 (accessed on 18 September 2018).

- Murray, B.C.; Newell, R.G.; Pizer, W.A. Balancing cost and emissions certainty: An allowance reserve for cap-and-trade. Rev. Environ. Econ. Policy 2009, 3, 84–103. [Google Scholar] [CrossRef]

- Liu, Z.; Liu, F.; Wang, Y.; Hao, H.; Zhao, F. Integrated Study and Combined Policy Suggestions on CAFC, NEV and Carbon Credits. Chin. J. Automot. Eng. 2017, 1, 1–9. (In Chinese) [Google Scholar]

- Zou, Y.; Chen, C.; Su, H. Development and Application of the Corporate Compliance Calculation Model in CAFC and NEV Credit Management. Auto Eng. 2017, 11, 50–53. [Google Scholar]

- Ou, S.; Lin, Z.; Qi, L.; Li, J.; He, X.; Przesmitzki, S. The dual-credit policy: Quantifying the policy impact on plug-in electric vehicle sales and industry profits in China. Energy Policy 2018, 121, 597–610. [Google Scholar] [CrossRef]

- Ministry of Finance (MOF) and Ministry of Science & Technology (MOST). Notice about the demonstration work of promoting energy efficient and new energy vehicles. 2009. Available online: http://www.most.gov.cn/fggw/zfwj/zfwj2009/200902/t20090224_67588.htm (accessed on 18 September 2018).

- Ministry of Finance (MOF) and Ministry of Science & Technology (MOST). Notice on pilot implementation of subsidies on privately purchasing new energy vehicles. 2010. Available online: http://www.miit.gov.cn/n1146295/n1146592/n3917132/n4061919/n4061921/n4061926/n4061927/c4173089/content.html (accessed on 18 September 2018).

- Ministry of Finance (MOF) and Ministry of Science & Technology (MOST). Notice on further promoting the adoption of new energy vehicles. 2013. Available online: http://www.gov.cn/zwgk/2013-09/17/content_2490108.htm (accessed on 18 September 2018).

- Ministry of Finance (MOF) and Ministry of Science & Technology (MOST). Notice on further enhancement of promoting the adoption of new energy vehicles. 2014. Available online: http://www.gov.cn/gzdt/2014-02/08/content_2581804.htm (accessed on 18 September 2018).

- Ministry of Finance (MOF) and Ministry of Science & Technology (MOST). Notice on fiscal policies of promoting the adoption of new energy vehicles during year 2016 to 2020. 2015. Available online: http://jjs.mof.gov.cn/zhengwuxinxi/zhengcefagui/201504/t20150429_1224515.html (accessed on 18 September 2018).

- Ministry of Finance (MOF) and Ministry of Science & Technology (MOST). Notice on adjusting and improving the financial subsidy policy for the promotion and application of new energy vehicles. 2016. Available online: http://jjs.mof.gov.cn/zhengwuxinxi/tongzhigonggao/201612/t20161229_2508628.html (accessed on 18 September 2018).

- MOF; MIIT; MOST; NDRC. Notice on adjusting and improving the financial subsidy policy for the promotion and application of new energy vehicles. 2018. Available online: http://jjs.mof.gov.cn/zhengwuxinxi/zhengcefagui/201802/t20180213_2815574.html (accessed on 18 September 2018).

- MIIT. Subsidies for New Energy Vehicles will Phase Down after 2020. 2018. Available online: http://www.xinhuanet.com/auto/2018-01/20/c_1122289000.htm (accessed on 18 September 2018).

- MIIT. New Energy Vehicles Exempted from Vehicle Purchase Tax: 10th–15th Batches. 2017. Available online: http://www.miit.gov.cn/n1146285/n1146352/n3054355/n3057585/n3057592/c5965520/content.html (accessed on 18 September 2018).

- MIIT. Manufacturers and Products of Road Motor Vehicle: 1st–12th batches in 2017. 2017. Available online: http://www.miit.gov.cn/n1146285/n1146352/n3054355/n3057585/n3057592/c5996875/content.html (accessed on 18 September 2018).

- Zhao, F.; Chen, K.; Hao, H.; Wang, S.; Liu, Z. Technology development for electric vehicles under new energy vehicle credit regulation in China: scenarios through 2030. Clean Technol. Environ. Policy 2018, 1–15. [Google Scholar] [CrossRef]

- MIIT, SAE-China. The technology roadmap for energy-saving and new energy vehicles. 2016. Available online: https://www.sohu.com/a/117879979_386926 (accessed on 18 September 2018).

- International Energy Agency (IEA). Global EV Outlook 2017; IEA: Paris France, 2017. [Google Scholar]

- Nykvist, B.; Nilsson, M. Rapidly falling costs of battery packs for electric vehicles. Nat. Clim. Chang. 2015, 5, 329–332. [Google Scholar] [CrossRef] [Green Version]

- EPA; NHTSA. Draft Technical Assessment Report: Midterm Evaluation of Light-Duty Vehicle Greenhouse Gas Emission Standards and Corporate Average Fuel Economy Standards for Model Years 2022-2025; U.S. EPA, NHTSA: Washington, DC, USA, 2016.

- International Council on Clean Transportation (ICCT). Passenger Car Fuel-Efficiency, 2020-2025 Comparing Stringency and Technology Feasibility of the Chinese and US Standards; ICCT: Washington, DC, USA, 2013. [Google Scholar]

- EPA; NHTSA. Joint Technical Support Document: Final Rulemaking for 2017-2025 Light-Duty Vehicle Greenhouse Gas Emission Standards and Corporate Average Fuel Economy Standards; U.S. EPA, NHTSA: Washington, DC, USA, 2012.

- Liu, Z.; Zhao, F. Insights on Automotive Industry; China Machine Press: Beijing, China, 2017; Volume 1. [Google Scholar]

- Liu, Z.; Hao, H.; Cheng, X.; Zhao, F. Critical issues of energy efficient and new energy vehicles development in China. Energy Policy 2018, 115, 92–97. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Class | Glider Weight (kg) | Technology Cost per % Electricity Consumption Improvement (yuan/%) | Incremental Technology Cost in 2020 (2017¥) | Incremental Technology Cost in 2025 (2017¥) |

|---|---|---|---|---|

| A00 | 800 | 448 | 3897.6 | 9676.8 |

| A0 | 1000 | 480 | 4176 | 10368 |

| A | 1200 | 512 | 4454.4 | 11,059.2 |

| B | 1600 | 576 | 5011.2 | 12,441.6 |

| C | 1800 | 608 | 5289.6 | 13,132.8 |

| D | 2000 | 640 | 5568 | 13824 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, K.; Zhao, F.; Hao, H.; Liu, Z. Synergistic Impacts of China’s Subsidy Policy and New Energy Vehicle Credit Regulation on the Technological Development of Battery Electric Vehicles. Energies 2018, 11, 3193. https://doi.org/10.3390/en11113193

Chen K, Zhao F, Hao H, Liu Z. Synergistic Impacts of China’s Subsidy Policy and New Energy Vehicle Credit Regulation on the Technological Development of Battery Electric Vehicles. Energies. 2018; 11(11):3193. https://doi.org/10.3390/en11113193

Chicago/Turabian StyleChen, Kangda, Fuquan Zhao, Han Hao, and Zongwei Liu. 2018. "Synergistic Impacts of China’s Subsidy Policy and New Energy Vehicle Credit Regulation on the Technological Development of Battery Electric Vehicles" Energies 11, no. 11: 3193. https://doi.org/10.3390/en11113193